Call Now

Call Now

Equifax Credit Score : What, How to calculate & apply for a Free Equifax Report and Score

If you have ever tried to get a high-end loan or credit card, the banks would have mentioned the term ‘credit score’/’credit report’. But, what is an Equifax credit score?

What is an Equifax Score?

Equifax credit score is a 3-digit number ranging from 300 to 900 that speaks of a consumer’s creditworthiness. A higher Equifax score illustrates good credit health, whereas a lower score states that you have defaulted or delayed your payments in the recent past. The potential lender checks for your score to know the probability of you paying the borrowed money back on time.

How is the Equifax Score Calculates?

Several factors are considered while calculating the Equifax score; repayment history is one of the significant factors in this case. Customer details such as credit activity, payments made on credit cards and loans, credit limit, age, number of credit accounts, types of credit accounts, the status of these accounts, and more are shared by banks and non-banking financial companies (NBFCs) are shared with Equifax. The shared data allows Equifax to provide accurate credit report and score, so the lenders can analyse the risk associated with every credit application.

How to Apply for a Free Equifax Report and Score?

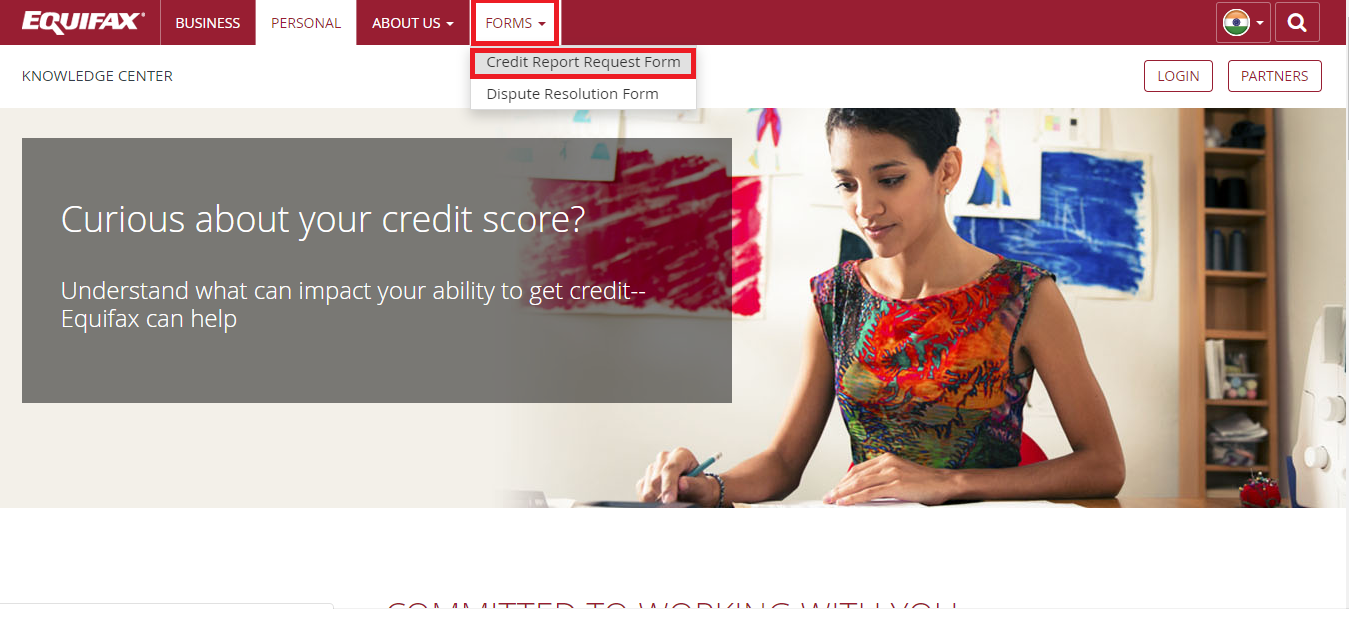

Step 1: Visit the official website of Equifax at https://www.equifax.co.in/personal/.

Step 2: Click on ‘Credit Report Request Form’ under the ‘Forms’ tab on the home page.

Step 3: You will be redirected to a page ‘Credit Report Request Form’ where you can download the request form. The page also specifies the list of documents that are required to get your credit report.

Step 5: Click on the PDF logo to download the form.

Step 6: Fill it up with relevant details and attach self-attested copies of the proofs you are submitting.

Step 7: Send the documents to Equifax’s address or through email to ecissupport@equifaxindia.com.

Is it Necessary to Access Equifax Report and Score?

It is recommended that you check the Equifax report often to make sure that the information pertaining to the finances being entered on your profile is valid and correct. This practice helps you to get rid of incorrect information that may have been saved in your profile. Errors in your report may cause a dip in your credit score, in turn, creates a negative impression to lenders about you. Similarly, personal information such as name, address, contact details, and others may also have errors leading to cases of fraud and ID theft; taking a look at your credit report often can help detect these errors.

Also, people with a low credit score can make efforts to improve their score by making payments on time. When this habit is maintained for a period of time, the score gets better. This can be confirmed by verifying the report often.

What does Equifax do?

Equifax, originally based in Atlanta, has a registered branch office in Mumbai, India as Equifax Credit Information Services Private Limited (ECIS). This credit rating agency has tied up with seven leading financial institutions such as State Bank of India, Religare Finvest Limited, Bank of Baroda, Kotak Mahindra Bank, Sundaram Finance Limited, Bank of India, and Union Bank of India. It has secured a licence from the Reserve Bank of India (RBI) similar to the other credit rating agencies.

Frequently Asked Questions

Does Equifax provide a decision if a person should get a loan or not?

No. Credit rating agencies such as Equifax does not provide a decision on if a person is eligible to get a credit facility or not. It only provides information on his credit history and lets the lender make the decision.

Is it not necessary that I register with Equifax to get the report?

Only people who are registered members of Equifax can get their credit report.

What should I do if there are errors in my credit report?

If you find errors on your credit report, you can raise a dispute with the agency using the dispute form available for download on the website. The agency consults the concerned financial institution to confirm the changes you have mentioned; it must correct the error within a period of 30 days from the date of request. If the changes turn out to be not acceptable, you will be informed on the same.

The loan availed earlier is not reflecting on the report. Why?

There may be cases when the loan you have taken earlier is not mentioned in the report. One reason can be that the lender of that loan is not a member of the bureau.

How long does a financial transaction stay on the report?

Any financial transaction you have made will stay on the credit report for a period of 36-48 months.

Related Articles

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption