|

Section 44 of CGST Act: GST Annual Returns Clause-by-Clause Explained

Section 44 of the CGST Act mandates filing of annual return i.e., GSTR 9 for all the taxpayers whose aggregate annual turnover exceeds Rs.2 Crore. The section also mandates filing of GSTR 9C which is a reconciliation statement which is to be filed by taxpayers with sales more This article provides you with an overview on Section 44 of the CGST Act, 2017.

Key Takeaways

- Section 44 ensures reconciliation of GST transactions of the entire financial year along with reconciliation statements for applicable cases.

- Filing return under the section provides the GST authorities a total picture of outward and inward supplies, tax paid, and ITC available and helps to match GST returns with books of accounts and detect mismatches.

- Perhaps, this helps to ensure that the taxpayers maintain proper records and avoid any misuse of the ITC claimed, for example, fake invoicing, bogus purchases, etc.

- GSTR 9 summarises the entire financial year’s GST transactions, verifying its accuracy.

What is Section 44 of CGST Act?

Excerpt from the provision CGST Section 44 is given below-

Let’s decode the Section 44-

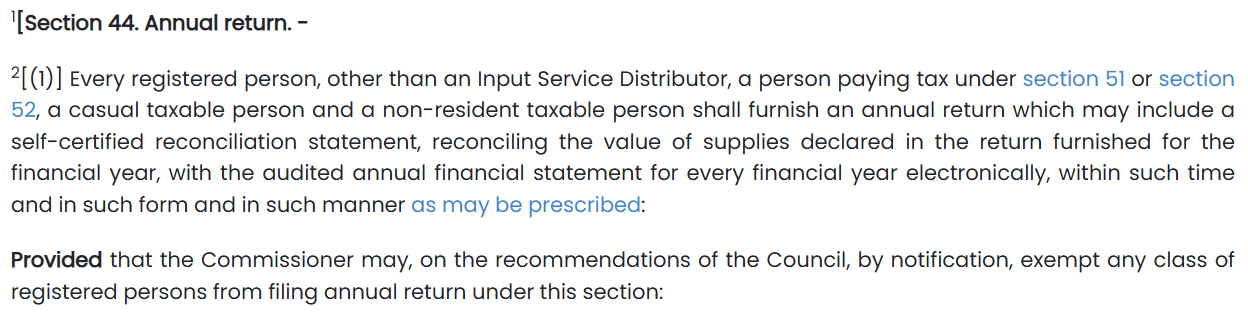

In simpler terms, every registered person, casual taxable person, non-resident taxable person must submit an annual return, which includes a self-certified reconciliation statement, reconciling the value of supplies declared in the return furnished for the financial year, with the audited annual financial statements for the financial year.

The commissioner has the authority to exempt any class of registered persons from filing an annual return, and the commissioner has exempted any department of the Central Government or a State Government or a local authority, whose books of account are subject to audit by the Comptroller and Auditor-General of India.

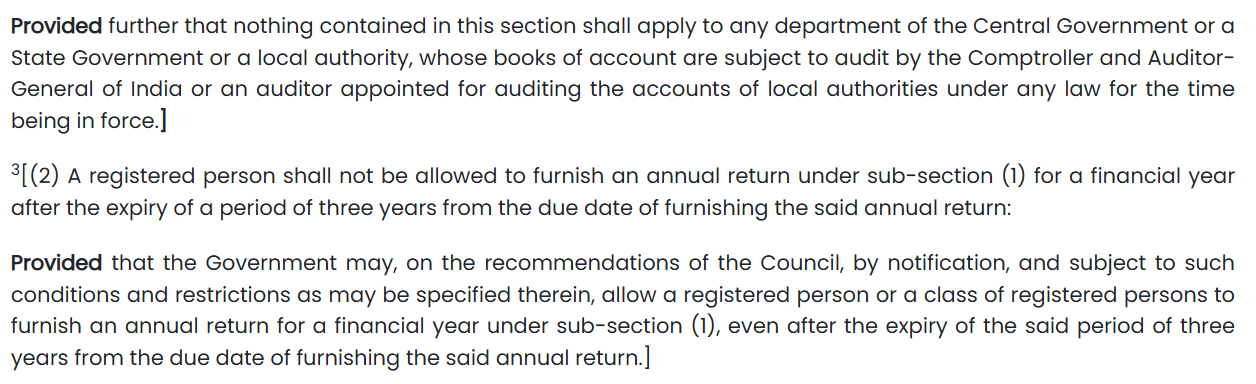

The Last date a registered person can file the annual return for a financial year is before the expiry of a period of three years from the due date of furnishing the said annual return.

Annual Return Filing under Section 44

The following are the features of Annual Return Filing as covered in the provision:

- Yearly Compliance – Every registered taxpayer (except specific exempt categories) must file the annual return by 31st December of the following financial year, summarising GST activities of the financial year.

Such a summary includes:

- Total Outward Supplies (Sales)

- Total Inward Supplies (Purchases)

- ITC Availed and Reversed

- IGST, CGST and SGST paid

- Monthly/Quarterly Reconciliation - The outward and inward supplies made every month/quarter must be reconciled with those of GSTR 9. Accordingly, adjustments to be made for all the inputs claimed that do not belong to the particular financial year or amendments made thereof.

- Categorise the Adjustments and Reconciliations Made - GSTR 9 contains the details of inputs under different tables:

- Table 6 contains the details of ITC claimed during the financial year in GSTR 3B of both regular and RCM cases.

- Table 7 contains the details of ITC reversed or lapsed during the financial year.

- Table 8 provides the reconciliation of ITC as per GSTR 2A/ 2B with GSTR 3B and books.

Applicability & Thresholds of Section 44

Section 44 applies to every registered taxpayer under GST who is required to file returns during the financial year. Thus, filing of annual return for all the taxpayers, except for the exemptions mentioned below:

- Input Service Distributor (ISD)

- GST TDS and TCS Collector

- Casual Taxable Person

- Non-Resident Taxable Person (NRTP)

- Person paying tax under section 52 (Collection of Tax by E-commerce Operators)

- OIDAR service providers

GSTR 9 - Annual Return for Regular Taxpayer

GSTR 4- Annual Return for Composition Taxpayers

GSTR 9B - E-commerce Operators TCS Collectors

GSTR 9C - Taxpayers with Sales Turnover more than Rs. 5 crores (Self Certified)

GSTR 9 filing applicability in different situations:

| Nil Transactions throughout the year | Nil GSTR 9 mandatory. |

| Cancelled GST during the FY | To be filed within the registered period. |

| Migrated/Transferred Business | To be filed for the period in which the GSTIN was active. |

Key Requirements & Compliances

Reporting Requirements – The annual return must include the year-wide details of:

| HEAD | DATA TO BE REPORTED |

| Outward Supplies | taxable, exempt, nil-rated, exports |

| Inward Supplies | Purchases from registered/unregistered persons |

| Input tax credit (ITC) | Claimed, reversed, lapsed, RCM |

| Taxes Paid | Cash and ITC utilisation |

| HSN-wise Summary | Mandatory based on turnover limit |

| Reverse-charge (RCM) | Whether or not from Registered/Unregistered Persons |

Penalties for Non-Compliance per day

The annual return is to be filed on or before the due date, which is 31st December of the following financial year.

If the return is not filed on the due date, then the following late fees will be levied:

- Rs. 100 per day per Act (CGST ₹100 + SGST ₹100), or

- Maximum late fees at 0.25% of turnover in the State/UT.

Common Issues & Challenges

- Elaborate data requirements

- Bifurcation of ITC into inputs, input services, and capital goods.

- HSN (Harmonised System of Nomenclature) and SAC (Service Accounting Code) summary for both inward and outward supplies.

- Input Tax Credit (ITC) Mismatches: This is a major issue, often involving discrepancies between the ITC claimed in GSTR-3B and the amount auto-populated in Table 8A of GSTR-9 (sourced from GSTR-2B/2A). Reasons include:

- Suppliers failing to file GSTR-1 on time or at all.

- ITC on inward supplies where the place of supply was reported incorrectly by the vendor.

- Invoices from a period when the recipient was under the Composition Scheme are not being reflected.

- Reconciliation: A methodical approach is required to reconcile the data across GSTR 1, 3B, and the auto-populated figures in GSTR 9 with taxpayers’ books of accounts.

- No Revised Return: GSTR 9, once filed, cannot be revised, but in extreme cases, if revision of the return becomes necessary, then it can be addressed through other means like DRC-03 with additional scrutiny and penalties.

Frequently Asked Questions

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption