Call Now

Call Now

CIBIL Credit Report : What is Credit score & How to check Credit score online

Most of us are familiar with the concept of borrowing and lending. You would have come across at least one person who often forgets to return the money that he/she borrows. This makes you think twice to lend to that person because of their forgetful nature. Similarly, lending institutions would like to issue loans and credit cards only to those who they deem creditworthy. CIBIL score is one of the significant metrics that is used by the credit institutions in India to measure an individual’s creditworthiness.

What is CIBIL Score?

CIBIL score is one of the most important factors that almost every financial institution check when they receive credit application from individuals. TransUnion CIBIL has affiliations with almost every bank to gauge the creditworthiness of millions of individuals and enterprises. A high CIBIL score denotes not only your excellent financial discipline but also your integrity. Every time you apply for a loan or a credit card, your recent score (last six months) is checked. Generally, any score above 700 is considered excellent, though some banks keep the bar high and some do not mind lowering the standard.

Who Computes the CIBIL Score?

TransUnion CIBIL is a credit bureau or credit information company, incepted in 2000, the first of its kind in India. The firm computes the CIBIL score of individuals based on the consumer information stored in their repository. They are known for their accuracy and transparency in the calculation of the score.

How to Check Credit Score?

Here is the procedure to check CIBIL score:

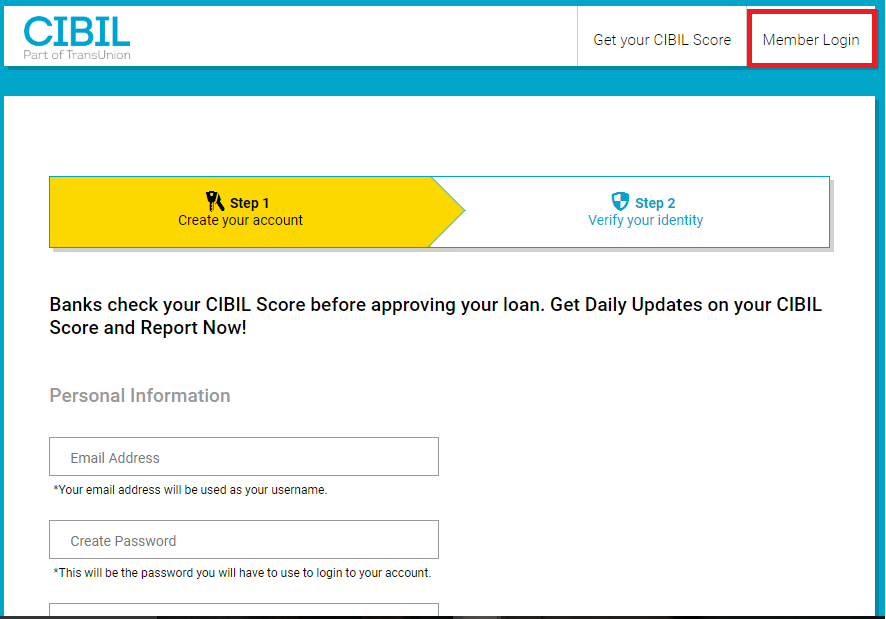

Step 1: Visit the official website of TransUnion CIBIL at https://www.cibil.com/freecibilscore.

Step 2: Under the ‘Personal’ tab, click on the ‘Get Yours Now’ button on the home page for a free CIBIL score. You can get a detailed report when you click on ‘Get Your CIBIL Score’ after paying certain charges applicable.

Step 3: Consider that you have opted for a free CIBIL score. You will be redirected to a page that prompts you to enter your personal information to sign up in the first step. The second step in signing up is to verify your identity with a government-issued identity proof document.

Step 4: If you already have an account, you can sign in to your account.

Step 5: Your credit score will be sent to you via the email address you have provided while signing up.

What are the Factors that Affect the CIBIL Score?

Repayment History

Banks and NBFCs consider lousy credit track record as an indicator of future behaviour. Every time you avail loan or credit, the lender is duty-bound to report it to CIBIL. The bank takes note of whether you repay the debt on time. If you make an effort to repay in advance, then it is seen as a positive sign. This shows that you can be trusted to repay the amount you owe.

Drastic Increase in Credit

As an earning individual, you may have a specific credit limit (whether it is for a loan or credit card). However, using them to the brim indicates credit hungry behaviour and banks see them as red flags. If you maintain a certain credit level each month, but suddenly seen spending significantly more, then it can result in a reduced score.

Debt to Income Ratio (DTI)

Generally, lenders don’t encourage people to take more debts, say around 40% of their income. So, DTI is used to gauge a loan applicant’s ability to repay based on his/her income. It is an excellent metric to inculcate financial discipline as well as to ensure that you can repay your future EMIs without feeling burdened.

Numerous Existing Loans

Having too many loans in your name will always be a matter of concern to lenders – like a home loan, a couple of personal loans, a vehicle loan and credit card(s) on top of them. It is always better to close one before availing the next. Focus on closing the smaller loans as soon as possible.

How to Get the CIBIL Report?

It is very easy to obtain your latest CIBIL score directly from the official website of TransUnion CIBIL.

Step 1: Every individual is allowed to check their CIBIL score for free once a year. If you have already used up this opportunity, then you need to select either of the paid plans below:

- 1-month Subscription – Rs.550

- 6-monthly Subscription – Rs.800

- 1-year Subscription – Rs.1,200

Step 2: Enter your personal details as requested in the online form.

Step 3: Enter the captcha shown in the box and check the box to accept the terms and conditions and proceed to the payment page.

Step 4: After making the payment and authenticating your account, you will receive the credit report in your mailbox within 24 hours.

What is the Importance of CIBIL Credit Score?

A CIBIL score is like a scorecard for your financial integrity. It is an indicator, which tells a lender either ‘yes, you can give the loan’ or ‘no, it doesn’t look like he/she will repay on time’. The following are the reasons why you should always keep your CIBIL score high.

For secured loan approval

There is a misconception that it is easy to avail secured finances such as home loans and auto loans, as you will be providing the lender with some security. However, your credit track record will still be looked into by the lender. This is how they decide on the upper limit and the interest rate. With a poor CIBIL score, the overall process can get complicated.

Quicker approval of unsecured loans

A clean chit from TransUnion CIBIL, when it comes to credit score, is of the utmost significance when you apply for loans without any security. Like personal loans, for instance. For a borrower with a high CIBIL score (say 750+), it is easier to get it sanctioned. If your score is above 800, then you might even get a higher amount than generally given by a bank.

More bargaining power on interest rates

Are you aware of the fact that the interest rates vary for different loans at different banks? Some people end up getting a better deal than others. A higher CIBIL score enables you to bargain with banks for a better rate or deal. You can easily compare the offers from lenders and authoritatively negotiate as creditworthy customers are assets for any financial institution.

A lesser premium for insurance

Insurance is another financial instrument that rides mainly on trust and credibility, whether it is life cover, medical insurance, or others. Your repayment history, claims history, and general handling of debts and dues – all these are tracked carefully by the insurance companies. This helps them determine if you can enjoy a lower premium compared to others policyholders with a low credit score.

Chance and choice to pick the best credit card

Credit cards, if used smartly, can give you a host of benefits. Though they allow a definite zero-interest period, the interest rates can shoot up drastically when you delay or miss a payment. With a better-than-good CIBIL score, credit card companies will vie with one another to give you the best possible deal. Otherwise, you can end up with a credit card with a ridiculously high-interest rate or a rejection.

Good Score and Bad Score

| CIBIL score | What it means |

| 850 – 900 | Shows that you have never defaulted even once and is an excellent score. |

| 750 – 850 | It is a fact that 79% of loans sanctioned are for people with 750+ score. Scores above 800 are considered high and you can easily ask for a lower rate on personal loans and credit cards. |

| 700 – 750 | A good score for secured loans. However, for unsecured credit, the bank might investigate further (like social score) or impose slightly higher rates. |

| 500 – 700 | This shows that you have delayed or defaulted a few times in the past. Personal loans can be difficult to obtain from a bank. A private financier may levy hefty interest. |

| 300 – 500 | Such poor score indicates too many discrepancies in past loan repayments to ignore. Unless you work on credit repair or improvements, it will be impossible for you to get a loan from any bank in the country. |

How to Improve CIBIL Score?

A bad credit score is not the end of the world. You can improve your score by doing the following. You need to note that it will take at least six months to see a considerable change in the credit score and ‘improvements’ on your credit report.

Avail your recent credit report

This will help you in understanding the current position and where you slipped. For instance, if it is a couple of delayed payments responsible for your low score, then you need to ensure that it doesn’t happen again. It will also help you in correcting errors, if any, or set a target (it has to be at least six months).

Never postpone payments

The number of procrastinators is on the rise, thanks to the dramatic advances in technology. However, CIBIL doesn’t buy this excuse, and you have to pay your dues and EMIs on time. If not, your score will fall. It is better to automate your payments to avoid unintentional delays.

Have a diverse credit-folio

This will act as proof to the lender that you are adept at handling different kinds of credit. Having a blend of secured loans (house loan, car loan) and unsecured loans (personal loan, credit card) can do that. A higher leaning towards unsecured loans is not looked upon favourably.

Don’t have unused credit cards

It is never a good idea to keep one or more credit cards idle. If you are scared of maximising the limit, use it for grocery shopping or fuel purchase and repay it at the beginning of next month, and if you do not want to use a particular credit card, then close it.

Smart handling of debts

If you are handling debts smartly, then the score will improve. For instance, we all know how a credit card works on revolving credit and can get unmanageable if we are not careful. In such a case, closing off credit card dues with a personal loan is a smart move. This means you pay less interest and can solve a problem quickly.

No maxing out the credit

Just because your credit card allows you to borrow up to Rs.2 lakh, doesn’t mean you do it. You need to ensure that you don’t upset the balance of debt-to-income ratio.

Not prolonging tenures

The tenure of the loan or credit is another factor that can impact your score. Say, if you have taken a personal loan with a tenure of three years, and have increased the tenure midway for a smaller EMI, it can cause your CIBIL score to drop.

Difference Between Credit and CIBIL Score

Credit Score

A credit score is a three-digit number that sheds light on how well an individual has handled credit in the past. In short, it shows individuals’ creditworthiness. In the modern world, it is very normal to avail credit for various purposes. Credit score can be considered as a progress report of your credit behaviour. Consistently good credit conduct fetches you a higher score (out of 900), while slip-ups will result in a lower score. It will be difficult for anyone to secure a loan of any kind, especially unsecured ones such as personal loans and credit cards with a low score. In case your application gets approved, then it will be at a higher interest rate than usual.

CIBIL Score

People often confuse credit score with CIBIL score. They wrongly use it interchangeably. The Indian Government has authorised four credit rating agencies to assess credit scores of individuals. They are; TransUnion CIBIL, Experian PLC, HighMark Federal Credit Union, and Equifax Inc. Out of these, TransUnion CIBIL is the most popular credit rating agency. CIBIL score is one of the most important factors that almost every financial institution check when they receive credit application from individuals. TransUnion CIBIL has affiliations with almost every bank, gauging the creditworthiness of millions of individuals and enterprises. A high CIBIL score denotes not only your excellent financial discipline but also your integrity. Every time you apply for a loan or a credit card, your recent score (last six months) is checked. Generally, any score above 700 is considered excellent, though some banks keep the bar high and some do not mind lowering the standard.

Frequently Asked Questions

What other credit agencies are functional in India?

The Indian government has authorised four credit reporting agencies including TransUnion CIBIL. The other three agencies are:

- Experian PLC

- HighMark Federal Credit Union

- Equifax Inc

What to do if there is an error in the credit report?

If you notice an error in the credit report you can dispute the error on the CIBIL website. Errors in multiple fields can be disputed in a single dispute.

How long does CIBIL take to resolve my dispute?

Upon submitting the dispute, it may take around 30 days for the organisation to resolve your dispute.

Does the score change if I get my credit report from any other agency?

There are possibilities for the credit score to change if you get the report from other unauthorised credit report agencies. This is because the proprietary algorithm to generate the credit report may vary from agency to agency.

Related Articles:

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption