|

FAQs on Invoice Management System (IMS) in GST

GSTN is scheduled to launch the new invoice management functionality IMS (Invoice Management System) on 1st October 2024 for ITC computation and claim process. This new feature will streamline many tasks for taxpayers, help reduce compliance errors, and change the future of GST compliance. It's natural for people to have questions.

FAQs on IMS in GST answer all the queries from the industry leaders to our representatives about this eagerly expected feature.

Basics of the Invoice Management System (IMS)

What is the Invoice Management System (IMS)?

The Invoice Management System, or IMS, is a dashboard functionality within the GST portal that streamlines communication of invoices and CDNs saved/submitted/filed by suppliers. It facilitates recipients' checking of the status of invoices and CDNs and provides the option to accept, reject, or keep them pending for a period in a single window.

When will IMS be made available to taxpayers?

GSTN will launch the IMS facility on the 1st October portal. However, from 14th October 2024 onwards, users will be allowed to take action on invoices/CDNs.

Which records will be available in IMS for taking action?

The IMS dashboard will make available the following records related to the invoices saved or filed by the suppliers through GSTR-1/1A/IFF.

- B2B - Invoices

- B2B - Invoices (Amendments)

- B2B - Debit Notes

- B2B - Debit Notes (Amendments)

- B2B - Credit Notes

- B2B - Credit Notes (Amendments)

- Eco [9(5)] Invoices

- Eco [9(5)] Invoices (Amendments)

However, invoices and CDNs that are not eligible for ITC because of the POS rules or as per Section 16(4) of the CGST Act will not appear on the IMS dashboard. The portal will auto-populate GSTR-2B with these missing invoice data directly under the 'ITC Not Available' section.

What documents will not be made available in IMS but will be part of GSTR-2B?

The following documents/records will not be a part of IMS. They will flow directly to the GSTR-2B of the recipient:

- Document flowing from forms GSTR 5 and GSTR 6

- ICEGATE documents

- RCM records

- Document where ITC is ineligible because of POS rules and Section 16(4) of CGST Act

- Documents where ITC is to be reversed on account of Rule 37A

Who will have access to IMS functionality?

- GST-registered normal taxpayers

- SEZ unit/SEZ developers)

- GST-registered casual taxpayers

As a taxpayer, what will I be able to view on the IMS?

As a taxpayer, you will have two separate view options inside the IMS:

- Inward Supplies - This is the recipient's view. All options related to taking actions on record will be available in this section.

- Outward Supplies—This is the supplier's view. Suppliers can check actions taken on their saved or filed records in this section.

Which invoices have been visible on the IMS dashboard since 14th Oct 2024?

GSTN launched IMS on 1st October, but users were allowed to upload documents from 14th October 2024. So, all invoices/records for the GSTR-2B period from the October 2024 return period onwards are available on the dashboard. Users will not be able to check records/invoices for any GSTR-2B period (like Sept 24, Aug 24, etc.) before October 2024.

Which is the first GSTR-2B prepared using actions taken on IMS?

The IMS will auto-generate the first draft of GSTR-2B for any users on 14th November 2024. It will be generated based on all actions a user took from 14th October 2024 for the GSTR-2B period of October 2024.

Can a taxpayer take action after 14th Nov 2024 and regenerate GSTR-2B of the Oct ‘24 return period?

Yes. A taxpayer can amend or take other actions after 14 November 2024 on invoices/records for the Oct 24 GSTR-2B return period and recompute their GSTR-2B in the portal. This is allowed until the taxpayer files their GSTR-3B for the Oct 24 return period.

Is it mandatory to act on IMS? What happens if no action is taken?

The GST portal considers records/invoices as ‘deemed accepted’ if users do not take action in the IMS within a GST return period for auto-generating GSTR-2B for taxpayers. So, acting on records/invoices in the IMS is not mandatory. However, in that case, inappropriate invoices will also be considered as ‘deemed accepted’, causing improper tax liability and compliance issues.

The IMS workflow

How can I access IMS?

- Log in to the GST portal.

- Access IMS following the following path: GST portal Dashboard > Services > Returns > Invoice Management System (IMS) Dashboard.

What will happen to the accepted and rejected records?

- Once accepted in the IMS, an invoice will become a part of GSTR-2B. The portal will auto-populate GSTR-2B and GSTR-3B with tax-paid details from the accepted invoice for the ITC claim.

- Once rejected in the IMS, an invoice will not become part of the GSTR-2B, and the portal will not auto-populate GSTR-3B with details of the rejected invoice.

- IMS at the supplier's end will show rejected invoices and allow the supplier to amend invoices through GSTR-1 (if not filed already) or GSTR-1A.

When GSTR-3B is filed for a period, all the accepted/rejected records (except records with PENDING status until the limit as per u/s 16(4) of CGST Act) related to that period will be removed from IMS.

When will the invoices/documents flow to IMS?

Invoices will appear in the IMS dashboard when suppliers save the documents in their corresponding GSTR-1/1A/IFF.

When can the recipient taxpayer take action on a record?

Recipient taxpayers can take action on an invoice or record as soon as it appears on their IMS dashboard.

What will happen to the documents in IMS when the recipient files GSTR 3B?

The system will remove all the accepted/rejected records belonging to a particular GSTR-2B from the IMS once GSTR-3B for the period is filed.

What will happen to the documents that are kept pending in IMS?

Pending records will continue to appear in the IMS until the timeline prescribed by section 16(4) of the CGST Act, 2017. Beyond the cut-off date, the system will remove them as those records will no longer be eligible for ITC.

What is the draft GSTR 2B?

Under the IMS facility, the system-generated GSTR-2B is considered a draft GSTR 2B. It is generated on the 14th of every month and contains accepted, deemed accepted, and rejected records. However, rejected records are view-only and cannot flow to the GSTR-3B.

Which documents will be considered for the GSTR-2B generation?

The system will consider all accepted, rejected and 'No Action' records for GSTR-2B.

- Accepted records will appear under the 'ITC Available' section of GSTR-2B

- Rejected records will appear under the 'ITC Rejected' section of the GSTR-2B.

- 'No action' records will be treated as 'Deemed accepted', and it will appear in GSTR-2B.

Can I take any action after the generation of draft GSTR 2B?

Yes. The system under the IMS facility will allow a recipient to take action even after the generation of the draft GSTR-2B, which is on the 14th of every month. The option is available until the date of filing the GSTR-3B or the due date of filing GSTR-3B. However, the user needs to recompute GSTR-2B for the actions taken after the 14th and file the same in GSTR–3B. The due date for GSTR-3B is the 20th of every month.

Is there any scenario where the system will not generate draft GSTR 2B on the 14th of the subsequent month?

Yes. The system will not generate a draft GSTR-2B by the 14th of a month if the user fails to file their GSTR-3B in the previous period. Once GSTR-3B is filed, taxpayers can generate their GSTR 2B from the IMS dashboard.

How many times can I regenerate GSTR-2B?

There is no restriction until the GSTR-3B is not filed within its due date.

What about GSTR-2B for quarterly taxpayers?

For QRMP scheme taxpayers, the system will not generate GSTR-2B for the 1st (M1) and 2nd (M2) months of quarters. For such taxpayers, the system will generate GSTR-2B (as a combined GSTR-2B for the entire quarter (M1, M2, and M3 combined)) on the 14th of the Q+1 month. So, for the first quarter of a FY, GSTR-2B will be system-generated on 14th July.

QRMP taxpayers will be able to recompute GSTR-2B after the 14th of the Q+1 month until the filing of the corresponding GSTR-3B. This is similar to the logic followed for monthly GSTR-2B / 3B.

What will happen to GSTR2A?

The IMS facility will not affect the generation of GSTR-2A. It will continue.

Is it mandatory to recompute GSTR 2B?

If a taxpayer takes action or changes records in the IMS dashboard after the generation of the draft GSTR-2B (14th of every month for normal and 14th of Q+1 for QRMP taxpayers), it is mandatory to recompute GSTR-2B.

Actions to be taken in the IMS

What are the actions that I can take on an IMS?

By default, all records in the IMS dashboard show a "No Action" status. Suppose actions are not taken within the time limit. In that case, the portal considers all records 'deemed accepted' at the time of GSTR-2B generation.

Actions that recipient users can take on any records on the IMS dashboard are:

- Accept

- Reject

- Pending

Are there any invoices/records where pending action is not allowed in the IMS?

As per the latest GSTN advisory dated 23rd September 2025, taxpayers can now keep the following specified records pending for only one tax period—one month for monthly filers and one quarter for quarterly filers:

- Credit notes, or upward amendments of credit notes

- Downward amendments of credit notes where the original credit note was rejected

- Downward amendments of invoices/debit notes only where the original was accepted and GSTR-3B filed

- ECO-document downward amendments where the original was accepted and GSTR-3B filed

This change provides taxpayers limited flexibility to delay action within the allowed timeframe.

Can I take action multiple times on a record/document in the IMS?

Yes. The IMS facility allows users to take action multiple times on an invoice/record before the filing of GSTR 3B for a period. For example, you may accept an invoice and save that status. Then, you may change your decision on that invoice and change the ACCEPT status to PENDING or REJECTED.

In case of multiple actions, the latest action will overwrite the last action taken by the user. The time limit for changing the previous action on an invoice/record is the recipient's filing of the corresponding GSTR-3B.

What will happen to documents/records/invoices/CDNs on which taxpayers have taken action on IMS?

As per different actions taken by the user:

- ACCEPT–The system will make accepted invoices/records part of the 'ITC Available' section of GSTR 2B and auto-populate GSTR 3B with accepted ITC records.

- REJECT–The system will list the rejected records in the 'ITC Rejected' section of the GSTR 2B. Records of rejected ITCs will not auto-populate GSTR 3B.

- PENDING–These records will not be part of GSTR 2B and GSTR 3B of any period. They will remain on the IMS dashboard until the user accepts or rejects the record or the end of the timeline as prescribed in Section 16(4) of the CGST Act.

- No Action–The system will consider these records deemed accepted at the time of generating GSTR-2B for the user.

What happens if the recipient rejects a record?

- If rejected before filing the supplier's GSTR-1, the supplier can edit and save the record. This changed record will appear in the recipient's IMS.

- If rejected after filling out the supplier's GSTR-1, the supplier will need to amend the rejected record by filing GSTR-1A. Suppliers can also file a new invoice with changed details (as per the recipient's reason for rejection) in the subsequent GSTR 1/ IFF. The amended record will appear in the recipient's IMS for action.

If the recipient rejects the tax invoice/debit note for supplies, which was reflected in GSTR-2B of Oct 24 as eligible for ITC, given that the last date to avail of ITC for FY 23-24 is Nov 30, 2024, what will happen?

- It is advisable to reconcile the records before filing the GSTR-1 for October before the due date, i.e. November 11 2024.

- The taxpayers can either accept or reject the record, after which the ITC for the rejected record won't flow to GSTR 2B for October. However, the recipient always has the option to change the action taken, recompute GSTR 2B, and take the corresponding ITC when filing GSTR-3B for October 24.

When should an invoice/debit note be rejected?

An invoice should be rejected when it is inappropriate or erroneous, and issuing CN and DN cannot solve the problem. However, it is essential to maintain the highest level of caution while rejecting a record/invoice in the IMS, as it will disallow claiming ITC for the rejected invoice for the recipient taxpayer.

In light of the time limit to avail ITC being till 30th November for FY 2023-24 or furnishing of annual return, whichever is earlier, how can the ITC of erroneously rejected invoice in IMS be taken by the recipient in the FY 2023-24?

If a user erroneously rejects an invoice in the IMS, they can change the action to ‘ACCEPT’ after the 14th of a month but before the due date of GSTR-3B filing. However, they will need to recompute the GSTR-2B to claim credit in the GSTR-3B for the return period.

Can a recipient accept a genuine credit note issued by a supplier in the IMS, as it will further reduce the recipient’s ITC? What if the recipient had reversed the ITC corresponding to the invoice itself because of 17(5), Rule 42, 38, 43, etc., or not availed the ITC at all because of POS or 16(4), etc., ineligibility?

As the recipient has already reversed the ITC for the said invoice, they can accept the CN without requiring reversal of the ITC again.

Amending records in the IMS

What happens to the original record if the supplier amends the same record?

It depends on the respective periods of the GSTR-2B for an original and its amended record.

- Different GSTR-2B period—The user must take action on the original record first, file the respective GSTR-3B, and then take action on the amended record later. Otherwise, the system will not accept the action.

- Same GSTR-2B period - Amended record gets priority, and its action will prevail over any action on the original record.

What will happen if I have taken action on a document in saved status but the same is edited/changed by the supplier before filing his GSTR-1?

If a supplier edits a saved record, even after the recipient has taken an action, the amended or changed record will replace the earlier saved document in the IMS. The system will reset the action taken by the recipient. So, the edited record will appear on the recipient's IMS dashboard 'No Action' record (will require a fresh action by the recipient).

Similarly, if a supplier deletes a saved record before filing a return, the record will be removed from the recipient's dashboard, irrespective of the action taken by the recipient.

How do you take action on the records available on the IMS dashboard?

- For individual records- Select the action by clicking any of the radio buttons A, R, or P at the line-item level corresponding to an invoice and clicking the save button.

- For multiple records - Select checkboxes for all the invoices you want to take action. The system will enable radio buttons for actions. You can select radio buttons at a go for all the selected invoices. However, only one type of action can be selected for taking action on multiple records.

Can a supplier amend an FCM invoice to an RCM invoice, and what will the impact be on the ITC?

Yes, as per GST law, the supplier can change an FCM invoice to an RCM invoice within a time limit. If the recipient accepts the FCM invoice, the system will reduce the recipient's ITC on the amended FCM invoice. Further, the RCM invoice will not appear in IMS and flow directly to the recipient's GSTR 2 B.

Can the supplier change the place of supply in the GSTR 1, and what will the impact be on the ITC?

Yes, the place of supply can be changed within the time limit per the GST law. If the change of place makes the supply ineligible for ITC, the recipient must reverse the ITC in Table 4B1 of GSTR-3B.

What will happen if the recipient rejects the original Credit Note or upward amended Credit Note?

If the recipient rejects the credit note, the system will add the corresponding liability to the supplier's liability in his/her GSTR 3B of the subsequent tax period.

What action shall be available on upward amended invoice/debit notes where the supplier only has saved the upward amended invoice/debit notes and the same is not filed?

The recipient can act on an upward amended record only when the supplier files the amended record using GSTR-1, GSTR-1A, or IFF. However, if the supplier only saves the amended record without filing it in the return, the recipient cannot take action on that saved amended record.

What should be done if a wrong invoice is corrected by issuing a credit note by the supplier instead of amending the same, and the recipient has rejected such a credit note?

Such a situation is one of the very few challenges of the existing IMS system. The supplier files an incorrect invoice and tries to rectify the mistake by issuing a CN. Suppose the recipient does not act on the invoice but rejects the CN. This will cause a mismatch in taxable value and liability in that case. Because not taking any action on the invoice will make IMS mark the incorrect invoice as deemed accepted. So, it is advisable to rectify mistakes in invoices/records by amendment through GSTR-1/GSTR-1A/IFF instead of issuing a CN.

In case of wrongly rejected invoices/ debit notes/ ECO-documents in IMS, how can a recipient avail ITC, if corresponding GSTR-3B of same tax period was also filed by him?

In such cases recipient can request to the corresponding supplier to report the same record (without any change) in same return period’s GSTR-1A or respective amendment table of subsequent GSTR-1/IFF. Thus, recipient can avail the ITC basis on amended record by accepting such record on IMS and recomputing GSTR-2B on IMS. Here the recipient will get ITC of complete amended value as original record was rejected by the recipient.

However, recipient will be able to take ITC for the again furnished document by the supplier, as stated above, only in the GSTR-2B of the concerned tax-period.

If any original record is rejected by the recipient and supplier furnishes the same record in GSTR-1A of same tax period or in the amendment table of GSTR-1/IFF of subsequent period, till the specified time limit, then what impact it will have on supplier’s liability?

In such cases supplier on noticing the same in the supplier’s view of IMS dashboard or on request of recipient, may furnish the same record again (without any change) in GSTR-1A of same tax period or in the amendment table of GSTR-1/IFF in any subsequent period, till the specified time limit, then the liability of supplier will not increase. As amendment table take delta value only. Thus, in present case of same values, differential liability increase will be zero.

As a recipient taxpayer, how to reverse ITC of wrongly rejected Credit note in IMS as the corresponding GSTR-3B has already been filed?

In such cases recipient can request the concerned supplier to furnish the same Credit note (CN) without any change in the same return period’s GSTR-1A or in amendment table of subsequent period’s GSTR-1/IFF. Now recipient can reverse the availed ITC based on the amended CN by accepting the CN on IMS. Hence, the recipient’s ITC will get reduced with complete amended value, as soon as the recipient recomputes GSTR-2B on IMS. The reduced value is same as that of the value of original CN as in this case the complete original CN was rejected by the recipient.

Can the Credit Note be kept as pending in IMS? If not, then why?

A recipient cannot keep a CN pending in the IMS because the supplier has already reduced tax liability on outward invoices for the GST return period by issuing the CN. However, a recipient can reject a CN if it is incorrect or does not belong to the recipient.

If any original Credit note was rejected by the recipient and supplier furnishes the same credit note in GSTR-1A of same tax period or in the amendment table of GSTR-1/IFF of any future tax-period, till the specified time limit, then what impact it will have on supplier’s liability?

At first instant the supplier’s liability will be added back in the open GSTR-3B return, because of original credit note rejection by the recipient. However, as the supplier furnishes the same credit note in GSTR-1A of same tax period or in amendment table of GSTR-1/IFF in any subsequent period, supplier’s liability for this amendment will get reduced again corresponding to the value of amended CN (which in this case is same as original). Thus, net effect on liability of supplier will be only once.

Can liability be added to the same month's GSTR-3B if the recipient rejects a credit note before the supplier files GSTR-3B?

No. The GSTR-3B for the same period will not change. Instead, the supplier's tax liability will increase in the subsequent period's GSTR-3B.

IMS Miscellaneous

Will Reverse Charge documents received from registered suppliers also form part of IMS?

RCM-related records/invoices will not be a part of the IMS dashboard. The portal will directly channel the RCM records data to the GSTR-2B.

Can I download all the data available in IMS?

Yes. All data in the IMS is available for download in Excel format.

New Changes in Invoice Management System (IMS) from October 2025 Tax Period

For which documents, pending option has been provided now which was not allowed earlier?

Pending option has also been provided for the following documents.

a. Credit notes, or upward amendment of Credit note,

b. Downward amendment of CN where original CN was rejected,

c. Downward amendment of Invoice / DN only where original Invoice already accepted and 3B has been filed,

d. ECO-Document downward amendment only where original accepted, and 3B has been filed.

What are the new changes being introduced in IMS?

- Taxpayers can now mark above records as Pending for action.

- Recipients can declare the Amount of ITC to be reduced for records where ITC was already reversed or not availed (e.g., CNs, amended CNs, or amended invoices/DNs).

- Recipients can now add remarks when marking records as Rejected or Pending.

Are these changes intended to be applied prospectively or retrospectively?

The new IMS features will apply prospectively from the October 2025 tax period.

Examples:

- CN dated 15 Sept 2025, filed in Sept 2025 GSTR-1 on 11 Oct 2025 → Appears in IMS without the new Pending option.

- CN dated 15 Oct 2025, filed in Oct 2025 GSTR-1 on 11 Nov 2025 → Appears in IMS with the new Pending option.

- CN dated 15 Mar 2025, filed in Oct 2025 GSTR-1 on 11 Nov 2025 → Appears in IMS with the new Pending option (GSTR-2B period: Oct 2025).

- CN dated 20 Sept 2025, filed in Sept 2025 GSTR-1A on 14 Oct 2025 → Appears in IMS with the new Pending option (GSTR-2B period: Oct 2025).

Till what date can Credit Notes and other specified records be kept pending?

Monthly taxpayers: 1 month

Quarterly taxpayers: 1 quarter

Records can remain pending until the GSTR-3B due date of the next tax period.

What will happen after the expiry of allowed period for keeping the record as pending?

Pending action will be disabled after specified period. Hence, recipient has to accept or reject that record after the expiry of specified time period. If no action is taken then system will consider such record as deemed accepted.

Will the taxpayer get any option to declare the amount of ITC which need to be reversed?

Earlier, the system automatically reversed the entire ITC in GSTR-2B upon acceptance of a credit note, even if the taxpayer had not availed or had only partially reversed the ITC.

From the October 2025 tax period, recipients can now declare the exact amount of ITC to be reversed for each record.

Upon accepting a record, the system will prompt:

“Whether ITC needs to be reduced for the selected record(s)?”

Recipients can choose:

No → No ITC reversal (e.g., ITC not availed earlier).

Yes → Full or partial reversal required.

If partial reversal is needed, the taxpayer can enter the ITC amount to be reversed (optional field).

If full reversal is required, selecting Yes without entering any value will auto-reverse the full ITC for that record.

The declared or system-computed ITC reversal will then reflect in GSTR-2B and be auto-populated in GSTR-3B.

Can I save the remark at the time of taking Reject/ Pending action?

Yes, at the time of taking Reject and Pending action on any of the record, taxpayer will get the option to save the remark. In case of Partial and no reversal remarks will be mandatory.

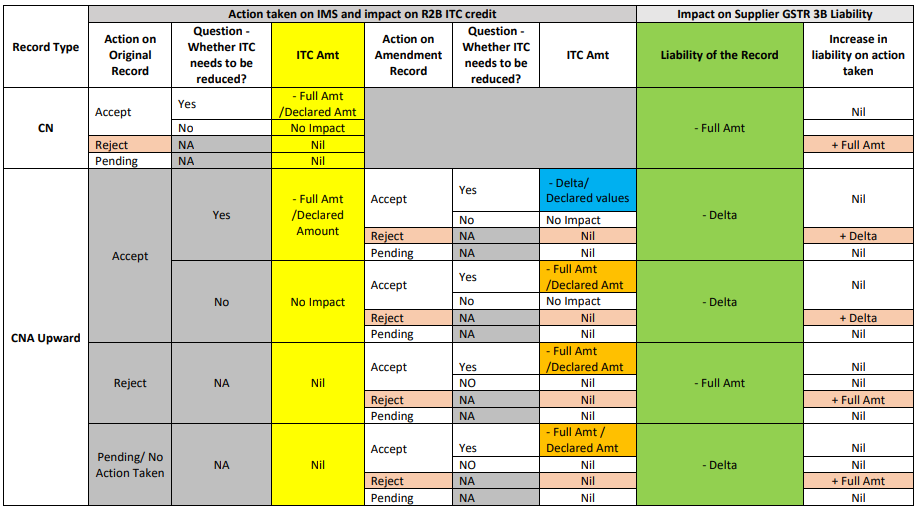

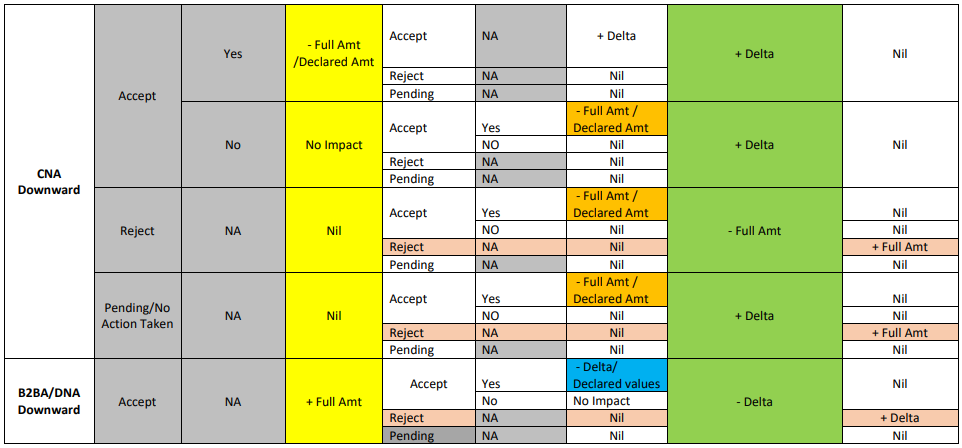

Actions taken on IMS and impact

Clear offers taxation & financial solutions to individuals, businesses, organizations & chartered accountants in India. Clear serves 1.5+ Million happy customers, 20000+ CAs & tax experts & 10000+ businesses across India.

Efiling Income Tax Returns(ITR) is made easy with Clear platform. Just upload your form 16, claim your deductions and get your acknowledgment number online. You can efile income tax return on your income from salary, house property, capital gains, business & profession and income from other sources. Further you can also file TDS returns, generate Form-16, use our Tax Calculator software, claim HRA, check refund status and generate rent receipts for Income Tax Filing.

CAs, experts and businesses can get GST ready with Clear GST software & certification course. Our GST Software helps CAs, tax experts & business to manage returns & invoices in an easy manner. Our Goods & Services Tax course includes tutorial videos, guides and expert assistance to help you in mastering Goods and Services Tax. Clear can also help you in getting your business registered for Goods & Services Tax Law.

Save taxes with Clear by investing in tax saving mutual funds (ELSS) online. Our experts suggest the best funds and you can get high returns by investing directly or through SIP. Download Black by ClearTax App to file returns from your mobile phone.

Office Address - Defmacro Software Private Limited, C 245A, Ground floor, Room No 1, Vikas Puri, West Delhi, New Delhi, Delhi 110018, India

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption