Call Now

Call Now

SARFAESI ACT, 2002- Applicability, Objectives, Process, Documentation

The SARFAESI Act, 2002 empowers banks and financial institutions in India to recover dues from defaulting borrowers without court intervention. The Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 plays a critical role in managing non-performing assets (NPAs) by allowing lenders to enforce security interests on secured loans through a legally defined process.

Key Highlights

- Applicable only to secured loans classified as NPAs under RBI guidelines.

- Allows possession, management, or sale of secured assets after a 60-day notice.

- Borrowers have the right to appeal before the Debt Recovery Tribunal (DRT).

- Certain assets and loans are expressly excluded from the Act’s scope.

What is the SARFAESI Act, 2002?

The SARFAESI Act, 2002 stands for the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002, It is a law that authorises banks and financial institutions to enforce security interests and recover non-performing assets without approaching civil courts.

- If a borrower defaults on a secured loan, the lender can seize and auction residential or commercial properties pledged as security, except agricultural land, which is exempt.

- The Act applies only to secured loans backed by assets such as mortgages, pledges, or hypothecation.

- For unsecured loans, banks must approach the civil courts to initiate recovery.

By streamlining the asset recovery process, SARFAESI helps reduce delays in handling defaults and improves overall credit discipline in the financial system.

Why was the SARFAESI Act Introduced?

The SARFAESI Act, 2002 was introduced to provide a legal framework for the securitization and reconstruction of financial assets, and for the enforcement of security interests by banks and financial institutions.

It was designed to facilitate faster recovery of loans and reduce the burden of non-performing assets (NPAs). The Act extends to the entire country and covers all matters related to or incidental to its main objectives.

Amendment

In 2016, the SARFAESI Act was amended through the Enforcement of Security Interest and Recovery of Debts Laws and Miscellaneous Provisions (Amendment) Act, 2016. This amendment aimed to strengthen the recovery process and improve the legal framework for debt resolution.

The 2016 amendment impacted four key legislations:

- The SARFAESI Act, 2002

- The Recovery of Debts Due to Banks and Financial Institutions Act, 1993 (RDDBFI)

- The Indian Stamp Act, 1899

- The Depositories Act, 1996

These amendments were made to streamline asset recovery procedures and enhance the effectiveness of secured lending in India.

Objectives of SARFAESI Act, 2002

The key objectives of the SARFAESI Act include the following:

- Efficient or rapid recovery of non-performing assets (NPAs) of the banks and FIs.

- Allows banks and financial institutions to auction properties (say, commercial/residential) when the borrower fails to repay their loans.

Who does the SARFAESI Act Apply to?

The SARFAESI Act, 2002 applies primarily to banks, financial institutions, and Asset Reconstruction Companies (ARCs). Below is a simplified overview of its scope:

I. Banks and Financial Institutions

- Can enforce secured loans without court intervention.

- Must classify borrower accounts as Non-Performing Assets (NPAs) as per RBI guidelines.

- Can appeal to the Debts Recovery Tribunal (DRT) and Appellate Tribunal if challenged.

II. Asset Reconstruction Companies (ARCs)

- Must be registered with the Reserve Bank of India (RBI).

- Can acquire financial assets from banks and issue security receipts to qualified buyers.

- Allowed to restructure assets, change management, or enforce security interests.

- Recognized as Public Financial Institutions under this Act.

III. Central Government Powers

- Can set up a Central Registry for transactions involving securitization or asset reconstruction.

- May extend the Act’s provisions to Non-Banking Financial Companies (NBFCs) and other entities.

IV. Scope Limitations

The Act does not apply to:

- Agricultural land

- Loans under ₹1 lakh

- Cases where 80% of the loan has already been repaid

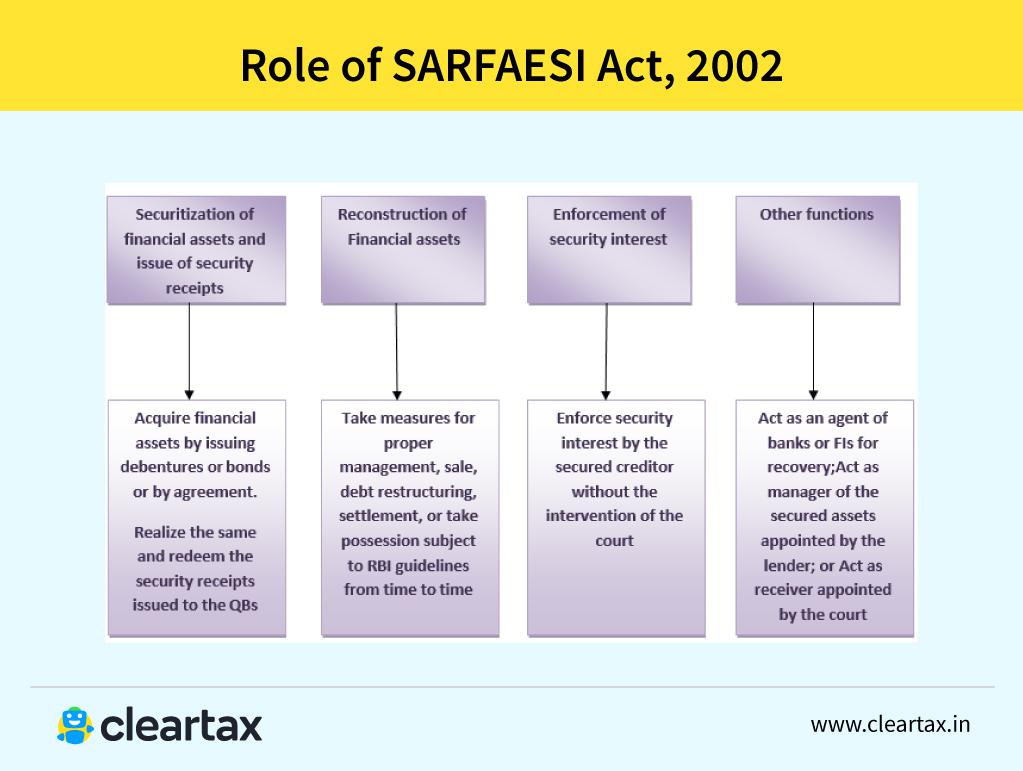

Role of SARFAESI Act, 2002

The SARFAESI Act, 2002 plays a critical role in strengthening India’s banking and financial system. Its key roles are outlined below.

How does the SARFAESI Act, 2002 Work?

SARFAESI Act, 2002 provides power to a bank or financial institution to seize the property of a defaulting borrower. If the loan borrowers make any default in repayment of a loan or a loan installment, the financial institution can classify the account as Non-Performing Asset (NPA).

The banks or financial institution can issue notices to the defaulting borrowers to discharge their liabilities within 60 days period. When the defaulting borrower fails to comply with the bank or financial institution notice, then the SARFAESI Act gives the following recourse to a bank:

- Take possession of the loan security

- Lease, sell or assign the right to the security

- Manage the same or appoint any person to manage the same.

The Act also provides for the establishment of ARCs, regulated by the RBI, to acquire assets from banks and other financial institutions.

Right of Borrower Under SARFAESI Act, 2002

The borrowers have the following rights:

- Borrowers can remit the dues and avoid losing their securities before the sale is concluded.

- Borrowers will get compensation for the default of an officer.

- SARFAESI Act Section 17 provides that borrowers can approach the Debt Recovery Tribunal to rectify their grievances against the creditor or authorised officer.

Amendments to the SARFAESI Act, 2002

The Enforcement of Security Interest and Recovery of Debts Laws (Amendment) Act, 2016 provided amendments for the SARFAESI Act, 2002 which are as follows:

- The banks and Asset Reconstruction Companies (ARCs) should have the power to transfer any part of the debt of the defaulting company into equity. Such a translation would indicate that lenders or ARCs would become equity holders, instead of the creditor of the company.

- Banks may request any immovable property set out for auction by themselves if they do not receive any request during the auction. In such a case, banks will be capable of adjusting the debt with the amount paid for this property. It allows the bank to secure the asset in partial fulfilment of the defaulted loan amount.

- Banks can also sell this property to a new person by asking him/her to remit these debts entirely over a period of time.

Methods of Recovery Under SARFAESI Act, 2002

The SARFAESI Act provides the following three methods of recovery of the Non-Performing Assets (NPAs):

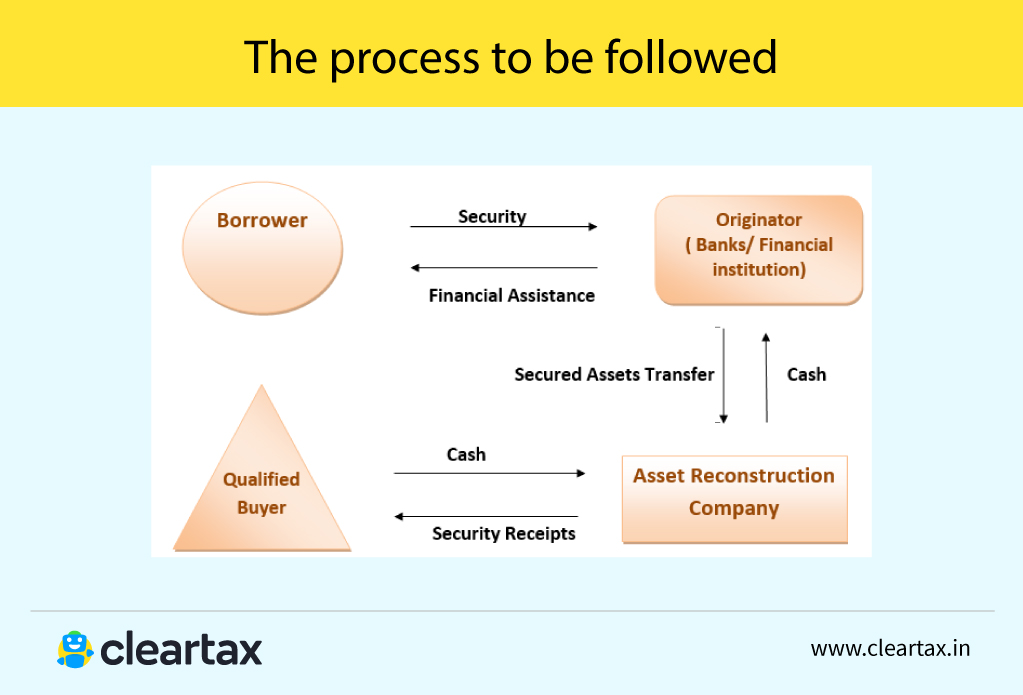

I. Securitisation

- Securitisation is the process of issuing marketable securities backed by a pool of existing assets such as home or auto loans. An asset can be sold after it is converted into a marketable security.

- A securitisation or asset reconstruction company can raise funds from only the Qualified Institutional Buyers (QIBs) by forming schemes for acquiring financial assets.

II. Asset Reconstruction

- Asset reconstruction empowers asset reconstruction companies.

- It can be done by managing the borrower’s business by selling or acquiring it or by rescheduling payments of debt payable by the borrower as per the provisions of the Act.

III. Enforcement of security without the interruption of the court

- The Act empowers banks and financial institutions to issue notices to individuals who have obtained a secured asset from the borrower for paying the due amount and claim to a borrower’s debtor to pay the sum due to the borrower.

Assets Not Covered Under SARFAESI Act, 2002

The SARFAESI Act does not cover the following assets:

- Money or security issued under the Sale of Goods Act, 1930 or Indian Contract Act, 1872.

- Any lease, hire-purchase, conditional sale, or any other contract where no security interest has been created.

- Any rights of the unpaid seller under Section 47 of the Sale of Goods Act, 1930.

- Any properties which are not liable for sale or attachment under Section 60 of the Code of Civil Procedure, 1908.

The SARFAESI Act, 2002 provides banks with a powerful legal mechanism to recover secured loan dues efficiently while balancing borrower rights. Understanding the SARFAESI Act, its applicability, recovery process, and safeguards helps borrowers and lenders navigate loan defaults and enforcement actions with greater clarity.

Frequently Asked Questions

Cleartax is a product by Defmacro Software Pvt. Ltd.

ISO 27001

Data Center

SSL Certified Site

128-bit encryption